- With food prices at historic highs, more consumers are turning to buy now, pay later services for their weekly essentials.

- "Once people start stretching out grocery payments it shows the height of personal desperation," says Marshall Lux, a fellow at the Harvard Kennedy School.

As prices rise, Americans are increasingly finding new ways to make ends meet.

But with some necessary purchases, such as groceries, there are fewer options that don't involve taking on debt.

We're making it easier for you to find stories that matter with our new newsletter — The 4Front. Sign up here and get news that is important for you to your inbox.

That makes the option to pay later — through companies such as Klarna, Zip, Zilch, Affirm and Afterpay — look increasingly attractive.

More from Personal Finance:

Most consumers underestimate monthly subscription costs

These steps can help you tackle stressful credit card debt

Americans now less likely to tip generously for takeout

About two-thirds of consumers have worried in the past month about affording groceries due to the rise of inflation, a recent LendingTree survey found.

Money Report

At the same time, Zip said it notched 95% growth in U.S. grocery purchases, according to The New York Times. Klarna reported that more than half of the top 100 items its app users are now buying are grocery or household items.

"The fact that there's a large number of Americans that simply can't afford to buy food highlights the desperation that this economic climate creates," said Marshall Lux, a fellow at the Mossavar-Rahmani Center for Business and Government at the Harvard Kennedy School.

"Once people start stretching out grocery payments it shows the height of personal desperation," Lux added.

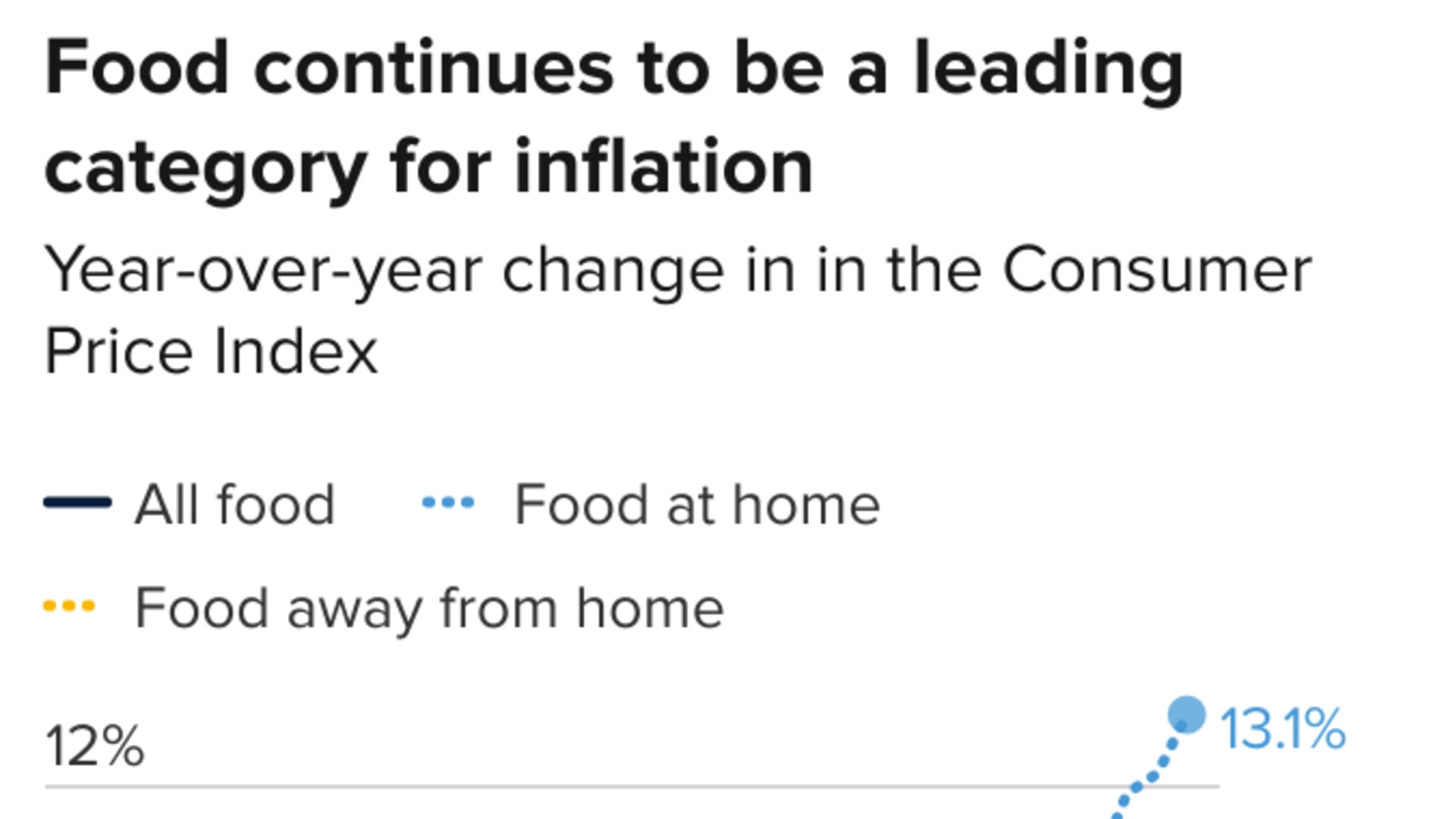

Although inflation, overall, began to ease last month along with gasoline prices, food costs climbed 1.1% in July, bringing the year-over-year gain to 10.9%, according to the latest Consumer Price Index figures.

The food-at-home index, a measure of price changes at the grocery store, notched the largest 12-month increase since 1979.

Using BNPL could mean people 'overextend themselves'

"For someone who has the ability to pay, this is an interest-free loan," Lux said.

However, BNPL's rapid growth is driven primarily by younger consumers, with two-thirds of BNPL borrowers considered subprime, Lux noted, which makes them especially vulnerable to economic shocks or a possible recession.

"In the best-case scenario, this will enable people to hang on or, in the worst case, overextend themselves," he said.

Further, the more BNPL accounts open at once, the more prone consumers become to overspending, missed or late payments and poor credit history, other research shows.

Generally, if you miss a payment there could be late fees, deferred interest or other penalties, depending on the lender. (CNBC's Select has a full roundup of fees, annual percentage rates, whether a credit check is performed, and if the provider reports to the credit scoring companies, in which case a late payment could also ding your credit score.)