Making a budget is one of the most important things you can do to set yourself up for success. And post-college graduation is a great time to start so you can build good money habits and watch your nest egg — and financial security — grow.

"If you don't understand what you have coming in and going out, there's no way to have a clear plan for your finances," explains Lauryn Williams, a certified financial planner, four-time Olympian and founder of Worth Winning, a company that provides financial guidance to young professionals. "You can calculate so many things and understand so much about what your financial goals are."

And, setting up a budget is a lot simpler than you think.

The key components of your budget are:

We're making it easier for you to find stories that matter with our new newsletter — The 4Front. Sign up here and get news that is important for you to your inbox.

Income: how much money you earn by working or through investments

Expenses:

- Fixed: any expense that is recurring and the amount largely stays the same (rent, utilities, loan payments, etc.)

- Variable: any expense that changes over time (gas, groceries, dining out, etc.)

Savings: what's left over when you subtract your expenses from your income

See? Not too complicated.

Whether you just graduated or you'll be graduating soon, here are a few tips to help you get started.

Money Report

What are your expenses?

First, you have to know what your expenses are — both fixed and variable.

Fixed expenses are easy to budget for since they are consistent costs.

It is "important to know your fixed costs going into each month," said Mary-Katheryn Egger, an accounting and retail management major at Syracuse University. "This way you always have the funds to cover those costs and know what is left over."

Variable expenses are a little trickier, because they may recur but they don't always and the amount fluctuates.

It can be hard to list out all the things you spend money on and how much you spend on each. If you're unsure, an easy way to see your routine purchases is to look at past transactions.

"I like to utilize my old bank account statements as reference to what I've spent in the past, and what my income has looked like," Egger explains.

Looking at your past statements is one of the easiest ways to see all your spending history in one spot. If you use a debit card, you should check your bank account statement, but a lot of credit cards also have some sort of a spending tool on their app that breaks down how much you're spending and where (gas, restaurants, entertainment, etc.). This will definitely help you in determining what your expenses are and how much you should be budgeting for each.

More from College Voices:

College Money 101: From student loans to setting up a budget

Quick tips to help college students start saving money

I want to move to New York after college graduation. Can I afford it?

A good rule of thumb is to over-budget for your variable expenses and see what's left over afterward rather than not having enough at the start. So, take a look at the past few months of your expenses. Figure out the average — say, if it's three months, add it all up and divide by three. Then, add a little extra.

Building and maintaining your budget

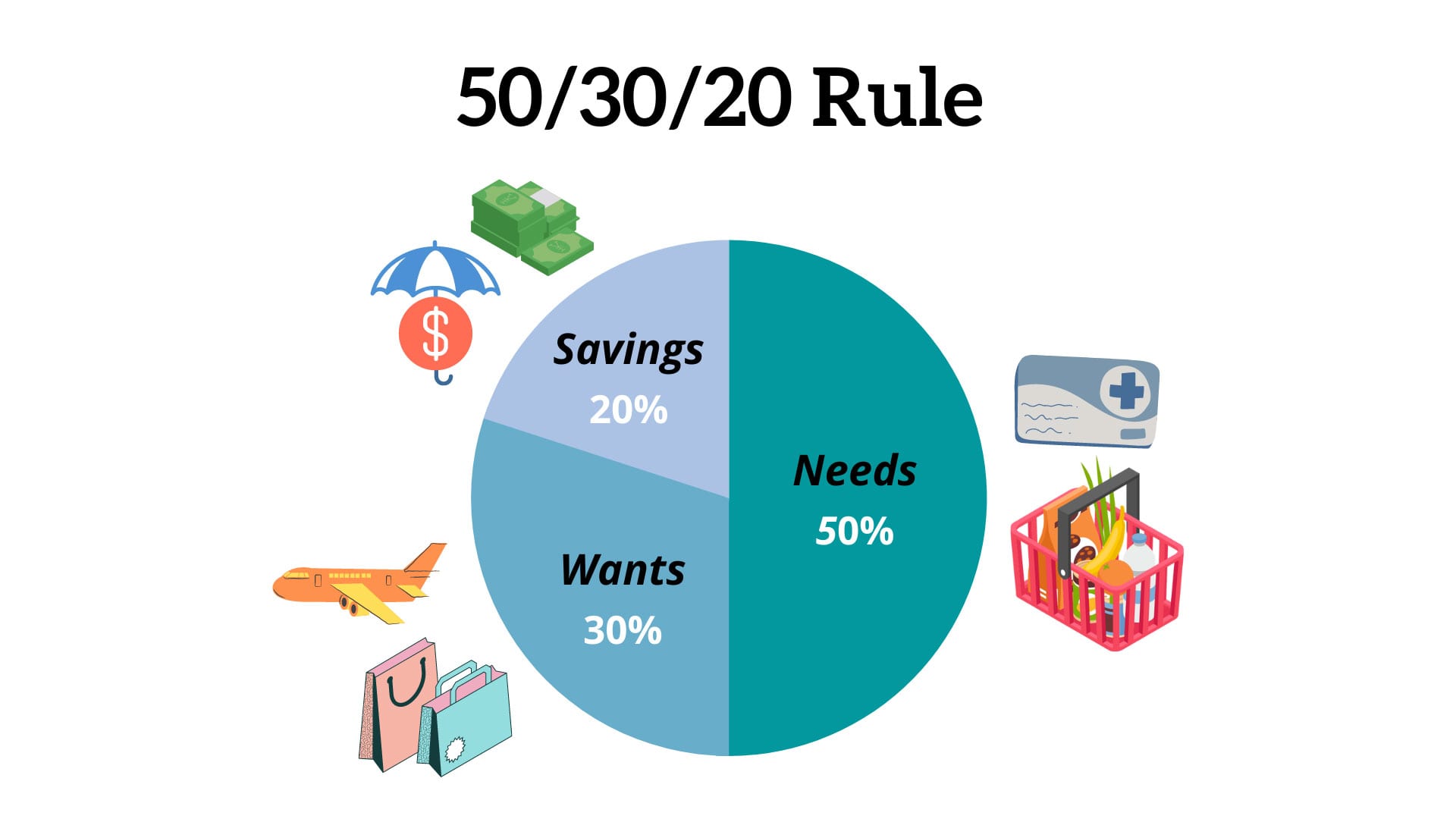

There are a lot of ways to set up a budget, but one of the most common approaches is called the 50/30/20 rule. That means: 50% of your income goes to your needs, 30% to your wants, and 20% to your savings.

Your needs and wants are essentially your expenses. Needs are the things you can't live without, like rent and groceries, and wants are things such as eating out, going to a baseball game or getting your nails done. And, you want to make sure that you are leaving enough left over for savings — some for unexpected expenses that may come up and also long-term savings.

Tools to help you stay on track

There are a lot of tools out there that can actually make budgeting a lot easier.

"I'm a big fan of technology giving us a lift to things that are boring and mundane," said Douglas Boneparth, a certified financial planner and founder of financial services firm Bone Fide Wealth.

Excel. Using an Excel budget sheet is one way to track your expenses. I found this free one online. It specifically breaks down costs not only by month but also by semester, which is helpful for those of us still in college. Then it weighs those against your income to find out if you are over or under. And here's the best part: We can leave all the math to Excel. The cells in this template already come with automatic calculations that make it possible for you to simply type in your numbers and Excel will do the rest. For example, if you're looking at the "Monthly Expenses" tab, when you alter those numbers — let's change $280 in rent to $300 — you'll find that the value of the G6 cell "what I spend" under the first tab ("Monthly Income") also changes. In this case, it'll increase from $920 to $940. Try it yourself and edit the sheet to your specific numbers.

Another route is manually creating your own budget sheet in Excel, which is exactly how Egger and Boneparth did it.

"I really appreciate being able to see a condensed version of my spending without having to log into online banking all the time," Egger said. "Also, I tend to add my own descriptions on my budget sheet, so I know what the purpose of each cost was." Creating your own sheet allows you to personalize your tracking and organize your finances in a way where you can best understand them.

Apps. Once you've grown comfortable with creating and managing your own sheet, you can apply these numbers anywhere. When Boneparth began budgeting his own personal finances on Excel, he "started to categorize expenses line by line" but realized it was "very laborious" and knew there had to be a more efficient way — and he's right. So, he opted to start using a budgeting app.

"Budgeting software can be very helpful. It's just getting into the routine and habit of taking a look at your expenses."

A few popular budgeting apps include Tiller, Mint and YNAB (You Need a Budget).

While starting your budget on Excel from scratch can give you a better and more detailed explanation of where your money is going, using budgeting apps adds a layer of efficiency that might be more useful for you.

There isn't a one-size-fits-all method to keeping track of your needs, wants and savings, so figure out which budgeting method works for you. Whether it's a template, a manual spreadsheet you created, an app, or a combination of those, you can choose what best suits you and your needs. You can even simply take a couple of minutes to jot down on your phone what you have and what you spend. And tracking your budget doesn't have to take up all your time. Dedicating just 10-15 minutes each day to tracking your spending will help you stay in tune with your money.

Are you living above your means?

If you find that you don't have enough left over for savings — or worse, if your spending is outpacing your income — then you are living above your means.

That is something that can happen easily — but you need to nip it in the bud now before you build a lifetime of bad habits. So, take a look at all of your expenses and see where you can cut back. The easiest place to cut back is on your variable spending — how much you're spending on groceries, eating out, going out, and buying things like clothing. But, if it's way over, then you should really take a hard look at some of your fixed expenses, such as rent and utilities — maybe you need to find a cheaper apartment or have fewer streaming subscriptions.

Mia DeVizio, a biomedical engineering major at Rutgers University, uses simple strategies in her daily life to save, such as choosing to eat in.

"I try to limit buying food and drinks because a lot of the time I can just eat something at home," DeVizio said. "This really saves me money, because eating out can really add up."

And sometimes, all you need to do is just take a second and think.

DeVizio's trick for preventing impulse purchases is to sleep on it. Waiting until the next day allows her to evaluate whether she really needs or wants the item, whether she can afford it and what the alternatives might be.

"I feel like 9 times out of 10 I realize that whatever I wanted wouldn't be worth buying," DeVizio said.

Let's talk savings

So, now knowing that you want to be saving 20% of your income, take a look at your numbers and see if what you have left over is, in fact, 20%.

"You're never going to buy a house unless you start saving," Boneparth explained. "It's extremely fundamental. You don't get to achieve these goals unless you get into the habit of saving and investing."

Now, if you're still in college, a house and 20% may seem out of reach. But you would be surprised how much all the things you assume you'll have one day — a house, a car, maybe a pool or nice vacations — will cost. And they are not guaranteed! So, you have to start building good habits now to get the life you want. And, remember: You're not just doing this for the long-term. Building good money habits will bring you wealth and help you do the things you want in the short-term, too.

Even if you don't have or make a lot of money, saving just a little bit now will do wonders for you in the future. You can start by setting a certain percentage aside from your paycheck, and then increasing that percentage as you make more. The path to financial independence and reaching your financial goals is to save, save, save.

Don't get frustrated if you don't make a lot. Or if you can't save a lot. Just start saving.

There are two big advantages to starting to save now, even if it's not a lot at first: 1) You are building a habit of saving that will help you build wealth, and 2) The sooner you invest your money, the more time it has to grow. Think of it like a tree: In one year, a tree grows a little. In 20 years, it grows a lot!

Expect the unexpected. If there's anything we've learned from the past two years, it's that the unexpected can happen — whether it's another pandemic or losing your job, you want to make sure you have something to fall back on just in case.

"Not being in control means you're going to be reactive, and that's a setup for failure. Flip it around: Get in control by understanding your numbers and being proactive with whatever headwind is coming your way," Boneparth said.

Your savings can and should act as an emergency fund.

How do you do that? You make sure that some of your money is "liquid," meaning you can access it quickly if needed. Maybe you need a new computer, or maybe it's medical expenses. These things don't wait for you to graduate or become financially stable. They can happen anytime. Whatever it is, things happen, and we don't have control over them. But we do have control over how we set ourselves up to be prepared for the unexpected. The most common ways to keep some of your cash liquid are through a checking account or a savings account linked to your checking account.

"A typical high yield savings account is totally fine," Williams said.

This is essentially the same as a regular savings account but with the added effect of a higher yield, meaning you'll earn more off your savings than you would with a traditional savings account. By opening a savings account, you can literally make money off what you already have.

And this isn't something you need a lot of money or a financial advisor to do. Just start researching online some options for high-yield savings account and compare your options — and the reviews. Make sure you only put your money with trusted financial institutions.

DeVizio uses a savings account and tries to keep a low amount of money in her checking account because she said it helps her avoid overspending.

And, to go back to that idea of liquidity, if an unexpected expense ever comes up, DeVizio can just transfer some money from her savings into her checking account.

Saving for retirement. If you are a recent college graduate, along with opening a savings account, contributing to your retirement fund is also something to consider. I know, we're just beginning to work so why are we already thinking about retirement? It's simple: We all want to stop working eventually. And, if you are in college and think this doesn't apply to you, think again! You will be graduating soon enough and be faced with these decisions. So, it's good to learn about them now and be planning for your future.

If you get a full-time job and your company offers a 401(k) plan, you should absolutely contribute to it as soon as possible and contribute the maximum you need to capitalize on any matching benefit your company offers. If you are freelance, start your own company or have a job that doesn't offer a 401(k), make sure you are saving on your own for retirement.

"I think retirement funds are extremely important to put savings into," Egger said. "I opened a Roth IRA as early as I could and it is one of the best financial decisions I've made," she said.

An IRA is an individual retirement account and is different from a Roth IRA, but nevertheless, both are great options. So, when you do stop working, your retirement funds will be there to give you a nice financial cushion where you can sit and thank your 20-year-old self.

Plan a money date ... with yourself!

Building your budget is nothing without tracking it. Check in with yourself routinely and see where you are in your finances.

Now, this doesn't mean no more fun and hours worth of looking at your budget. It doesn't have to be a long time, just a check-in to make sure you are on track. If you're not, make some adjustments.

"I found that setting aside time each Sunday for a budget review has proven very helpful," Egger said. "Having even a half an hour to look at your account history from the week and track what you've been spending ensures that you're never caught off guard by your account."

There's nothing worse than looking at your bank account and being greeted with a balance that's way lower than you expected, right?

Don't expect to get it right the first time.

When Egger first started managing her finances, she noted that it "came down to trial and error at first." She saw what worked and what didn't for her. Don't be a perfectionist. Go easy on yourself. Just start trying to budget — and stick with it, even when you mess up.

We've all heard the phrase: Practice makes perfect.

"You get good at something by practicing," Boneparth said. "So getting your budget right one or two months, even three, and saving a little bit, is that really a demonstration that you got this? Show me over a year, over two years."

You won't master your budget in one night, and that's OK. What matters most is that you keep at it.

Budgeting can help you reach your goals

Your financial goals are just as important as your personal ones. Budgeting will help you achieve both!

"By setting up a budget, you have a plan in place. You now can say, "OK, here's what I have as income. Here's what I have as expenses. Here's what my goals are. Here's what my savings goals are,'" Williams says. Having a budget will lay everything out for you.

"If you want financial success, it's really simple ... I'm gonna save $500 a month because I want to buy a car that costs $6,000. By having a budget, you know exactly, 'Oh, I get paid twice a month every month, I put away $500, I will have $6,000 12 months from now.'"

Purchasing a car or becoming a homeowner can have a hefty price tag. By budgeting, you can create measurable goals while staying within your limits. And, there's a real advantage to starting a budget when you don't have a lot of money.

"You don't have a whole lot so you learn how to budget with not a lot, and then the concept is the same when you do. As your money grows, you'll be able to manage it easily because you already have a plan in place," Williams said.

Budgeting can seem like a scary and tedious job at first even though it's really not. You have a lot of the tools and resources ready at hand to begin. Use the internet and your friends and family — these are all sources that can and want to help you. By creating, understanding and maintaining a steady budget as a college student, you're one step closer to reaching financial success.

″College Voices″ is a guide written by college students to help young people learn about important money issues such as student loans, budgeting and getting their first apartment. Sabrina Jeon is a rising senior at Lehigh University, majoring in marketing with a minor in mass communication. She is currently an intern for CNBC's direct-to-consumer marketing team, supporting the subscription services for CNBC Pro and The Investing Club with Jim Cramer. The guide is edited by Cindy Perman.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox. For the Spanish version, Dinero 101, click here.

CHECK OUT: I went from making $15 an hour to a net worth of $275,000 in 6 years: Here's how with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.