Investors should be able to take advantage of bullish momentum in tech stocks for at least the next couple of months.

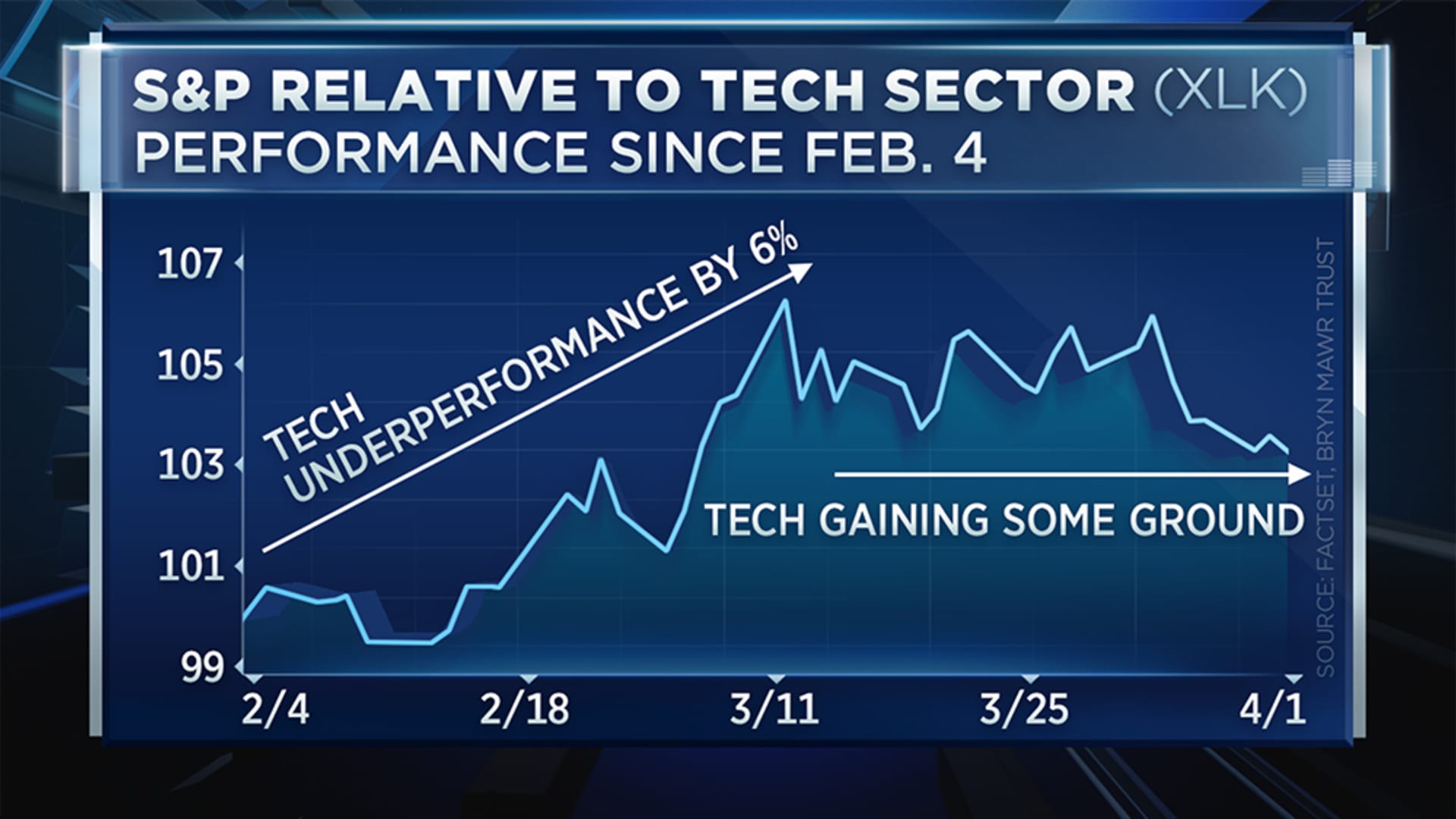

In my last post on the subject on Feb. 4, the takeaway was "tech's reign of relative dominance has come to an end." The tech sector as measured by the XLK ETF went on to trail the S&P 500 by about 6% over the next month, and growth trailed value by over 14% during that same period.

This is not meant to be a victory lap; far from it. A month of underperformance hardly meets the criteria for a loss of dominance. Further, the weakness of tech and growth stocks has started to reverse of late, clawing back about half of that initial underperformance.

We're making it easier for you to find stories that matter with our new newsletter — The 4Front. Sign up here and get news that is important for you to your inbox.

With stocks like Apple, Facebook, and Amazon trading down to their 200-day moving averages, what's next? Is tech ready to make a comeback, or is this just a pause along the road of further underperformance? I believe it is the latter.

This isn't your grandfather's momentum

Money Report

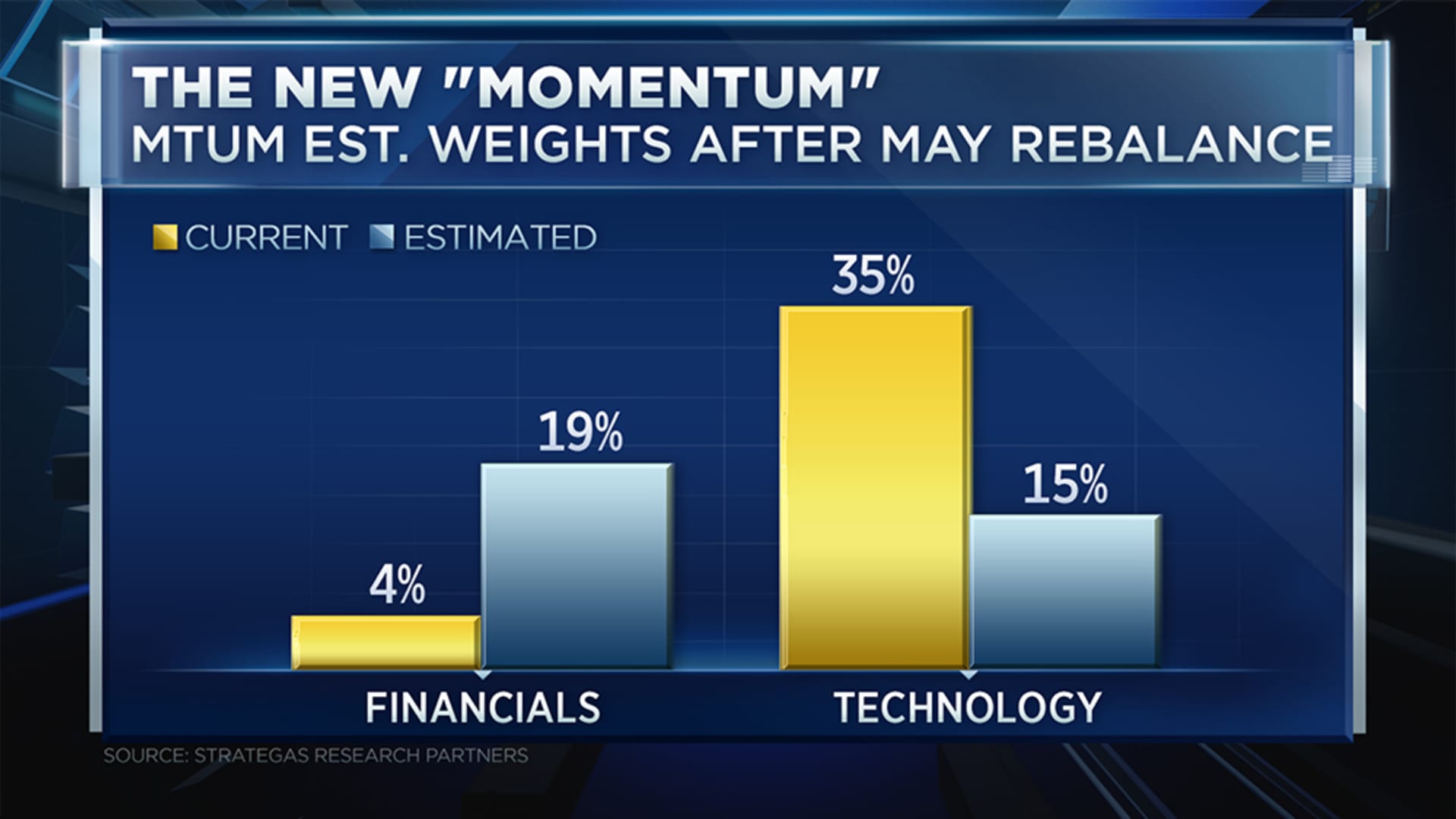

In recent years, technology stocks have been synonymous with momentum. Today, tech accounts for nearly 35% of the widely tracked iShares Momentum ETF (MTUM). This is about to change.

MTUM will rebalance during the last week of May, and the weighting to technology will likely be cut in half. Estimates forecast that financials, consumer discretionary, and industrials will carry the largest weights, and with that, additional flows will likely be attracted to those sectors.

This simple reconstitution is yet another catalyst for further underperformance from technology. Those that want exposure to momentum, whether through a passive ETF or an actively managed strategy, will by rule be owning less tech and more value. In fact, given tech's heavy weighting in most indexes, every 1% rotation out of "growth & defensive" sectors is nearly a 3% increase into "cyclical" sectors.

Valuation difference: hardly a dent

Although the tech sector's underperformance in 2021 has been noteworthy, it hasn't made a dent in the historically wide valuation difference between growth and value stocks.

Let's not forget that over the past 10-years, growth has outperformed value by an average of 7% per year. I think many investors still haven't come to terms with the idea that value can outperform for an extended period.

As I wrote in February, "The problem is that current prices [for growth stocks] necessitate a level of future growth that will be very difficult to realize". I still believe this to be the case. For example, Zoom is down 43% from its all-time high, but the stock still trades at 84x next year's earnings. Tesla is similar, down 23% from its high, but still trades at 145x forward earnings.

Value's outperformance this year has only driven the price-to-earnings premium in the tech-heavy growth index back to 2-standard deviations above normal. We have a long way to go before the valuation gap normalizes.

Interest rates: a (short-lived) opportunity for tech

Interest rate movements have been the primary driver of relative performance between growth and value.

Days when interest rates are rising, growth and technology struggle relative to value and cyclicals. I believe it is likely that interest rates drift sideways to lower in the coming weeks, allowing oversold conditions in certain tech names to adjust.

First, the interest rate differential between treasuries and many international government bonds is starting to attract foreign buyers to U.S. debt. European and Japanese buyers can earn an additional 1.2% by purchasing 10-year U.S. government debt versus 10-year bunds or JGBs, even after adjustments for currency risk.

This increased demand may serve to compress U.S. rates for a period. Additionally, sentiment has become extreme regarding U.S. treasury bonds — usually a good contra indicator. The percentage of bearish bond investors (betting rates will rise) is in the 90th percentile, and the 6-month rate of change in the 10-year yield is in the 97th percentile.

A normalization of sentiment would be another headwind to rising rates in the near term. With several large tech names at technical support, and investment flows into technology (as measured by XLK) weak, we could be due for a near-term reversal in performance leadership as the momentum higher in interest rates wanes.

However, it's unlikely to last. As foreign economies begin to ramp up vaccination efforts and their economies more fully reopen, their interest rates should rise as those bond markets anticipate higher growth and inflation.

The interest rate gap should narrow, making U.S. debt relatively less attractive to foreign buyers – less demand, lower prices, higher rates for treasuries. Further, the Federal Reserve has yet to push back against rising long-term interest rates, and the 10-year yield doesn't hit technical resistance until to the 2.0% to 2.25% range.

Taken together, U.S. rates should resume higher as we move into the second half of the year, creating a persistent headwind for tech's relative performance.

It's not all bad

It is important to keep in mind that this is relative performance story … not one of technology crashing and burning. The stock market today remains remarkably broad, with 96% of the stocks in the S&P 500 above their 200-day moving averages. The last time we saw a reading this high was late-2009. And even though technology has lagged, 90% of tech stocks are in an uptrend.

We know from history that rates and stocks can rise together. Even rates and technology stocks can rise together (see 2013 as an example). However, in the game of relative investment performance, my view remains that tech continues to fall behind.

Disclosure: Jeff Mills' firm Bryn Mawr Trust owns Apple.